2-hour backtest at 2 cycles per day, compared against the open-source LF Energy RTC-Tools benchmark.

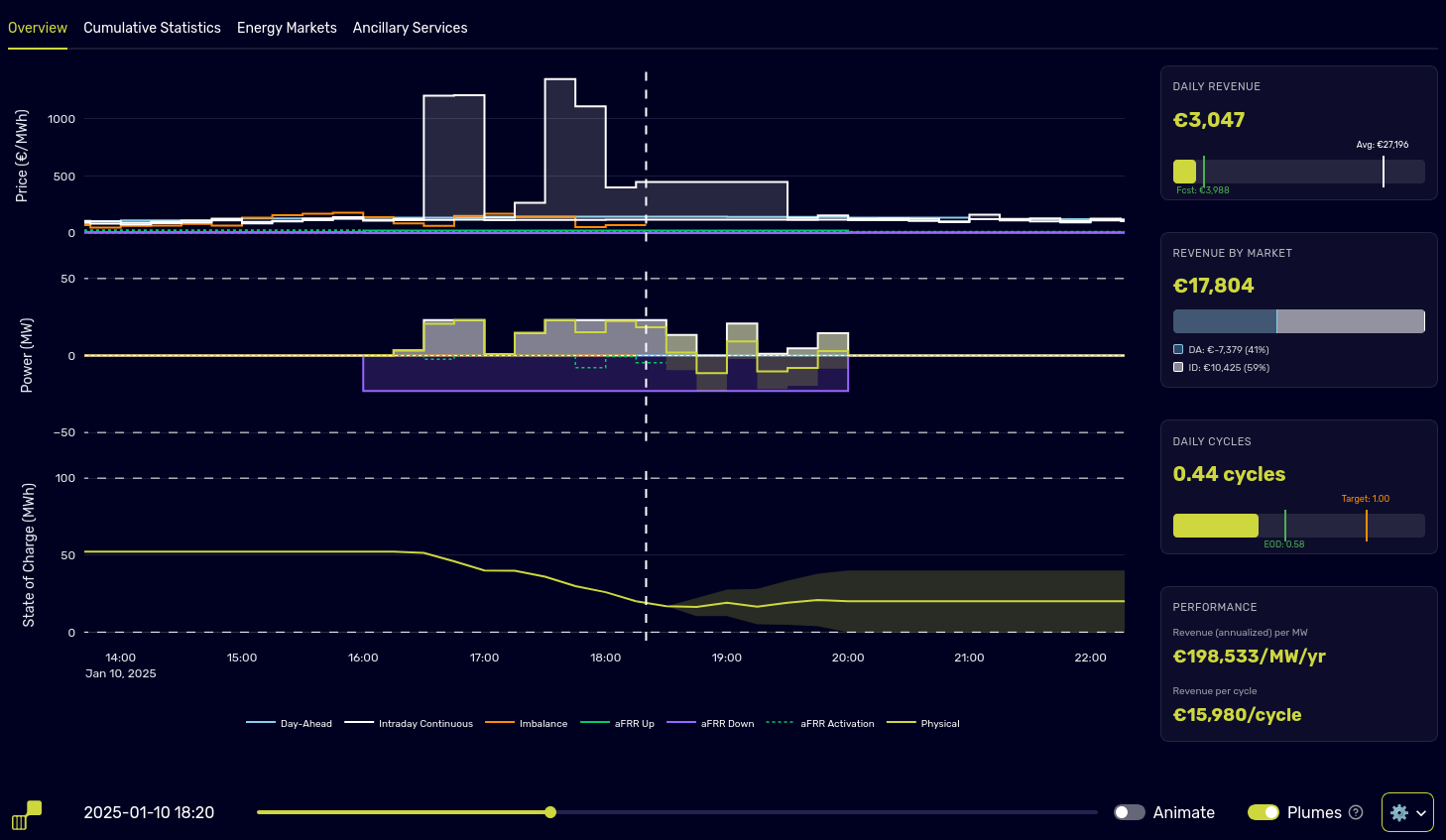

Overview view: energy market prices with aFRR capacity prices (top), co-optimised day-ahead, intraday, and ancillary power allocation (middle), state of charge trajectory (bottom).

Market Coverage

Every layer of the European value stack, captured in one optimisation

Day-Ahead Auctions

Participates in European day-ahead auctions (EPEX, Nord Pool, OMIE and others). Optimal charge and discharge scheduling across 24 hours.

Intraday Continuous

Trades continuously on European intraday order books (XBID and equivalents), responding to price movements as they develop. Order timing and sizing are optimised to avoid market impact while capturing available spreads.

Intraday Auctions

Participates in European intraday auctions (e.g. EPEX IDA3, Nord Pool IDA) to refine the schedule closer to real time.

Ancillary Services

Co-optimised participation in frequency containment reserve (FCR), automatic frequency restoration reserve (aFRR), and other ancillary services where available for the asset's market area.

One Engine, Every Market

The same optimisation engine runs across the whole of Europe — there is no country-specific fork to maintain. Local specificities — bidding zones, auction schedules and gate closures, product definitions, ancillary-service rules, and grid-code requirements — are configured per market and handled natively. Live today in Germany and the Netherlands.

Built for Real-World Complexity

Your network limits, contracts, and structures — handled in the optimisation, not bolted on

Local Network Constraints

Connection-point import and export limits, grid-connection constraints, local congestion, and shared-connection arrangements are all considered in the optimisation. Every schedule and order is shaped to what your grid position can realistically deliver — each cycle, automatically.

Flexible Offtake Structures

Merchant, tolling (physical or financial), revenue-share, or hybrid — trading is shaped to the commercial structure your asset operates under. Honour a toller’s dispatch rights, or optimise the merchant residual the structure leaves to you.

Virtual BESS (VBESS)

Work both sides of a virtual battery. Offer a VBESS — carving a physical asset or portfolio into independently optimised virtual units — accepting counterparty nominations and optimising the merchant residual around them. Or nominate into someone else’s VBESS construct, trading your contracted slice.

Ramp-Rate Limits

Inverter and grid-code ramp limits cap how fast your asset can swing between charge and discharge. The optimisation respects each unit’s maximum ramp rate when building day-ahead schedules and placing intraday orders, so every position is physically deliverable.

Not a Black Box

Open-Core

Built on the open-source LF Energy RTC-Tools framework. Every optimisation decision is auditable and explainable — no magic, no lock-in.

Fits Your Stack

Integrates via REST API into your existing systems. Use your own price forecasts or third-party providers; we enhance them and return optimised schedules and trade instructions.

Always Solves

Mathematical optimisation engines don't always converge to a feasible solution — or converge in time. Our proprietary low-level solver technology guarantees a solution on every auction and dispatch cycle, so your asset is never left without a schedule.

Proven in Europe

Live in Germany and the Netherlands. In the Netherlands, we delivered a 30% uplift in intraday trading revenue for a customer versus their prior approach. German results are benchmarked against published indices — see the 2025 performance data below.

Performance Evidence

Partner Ecosystem

The European Value Stacker plugs into leading trading platforms and consumes best-in-class price forecasts

Ready to Stack More Value?

Contact us to discuss your asset, target markets, and pricing.